Indian markets rebounded modestly on February 20, 2026, closing the week with marginal gains as selective buying in banks and metals helped offset early pressures from geopolitical tensions and elevated oil prices. Strong domestic PMI data, renewed FPI inflows, and positive AI-sector developments underpinned cautious optimism, despite lingering IT weakness and global trade uncertainties.

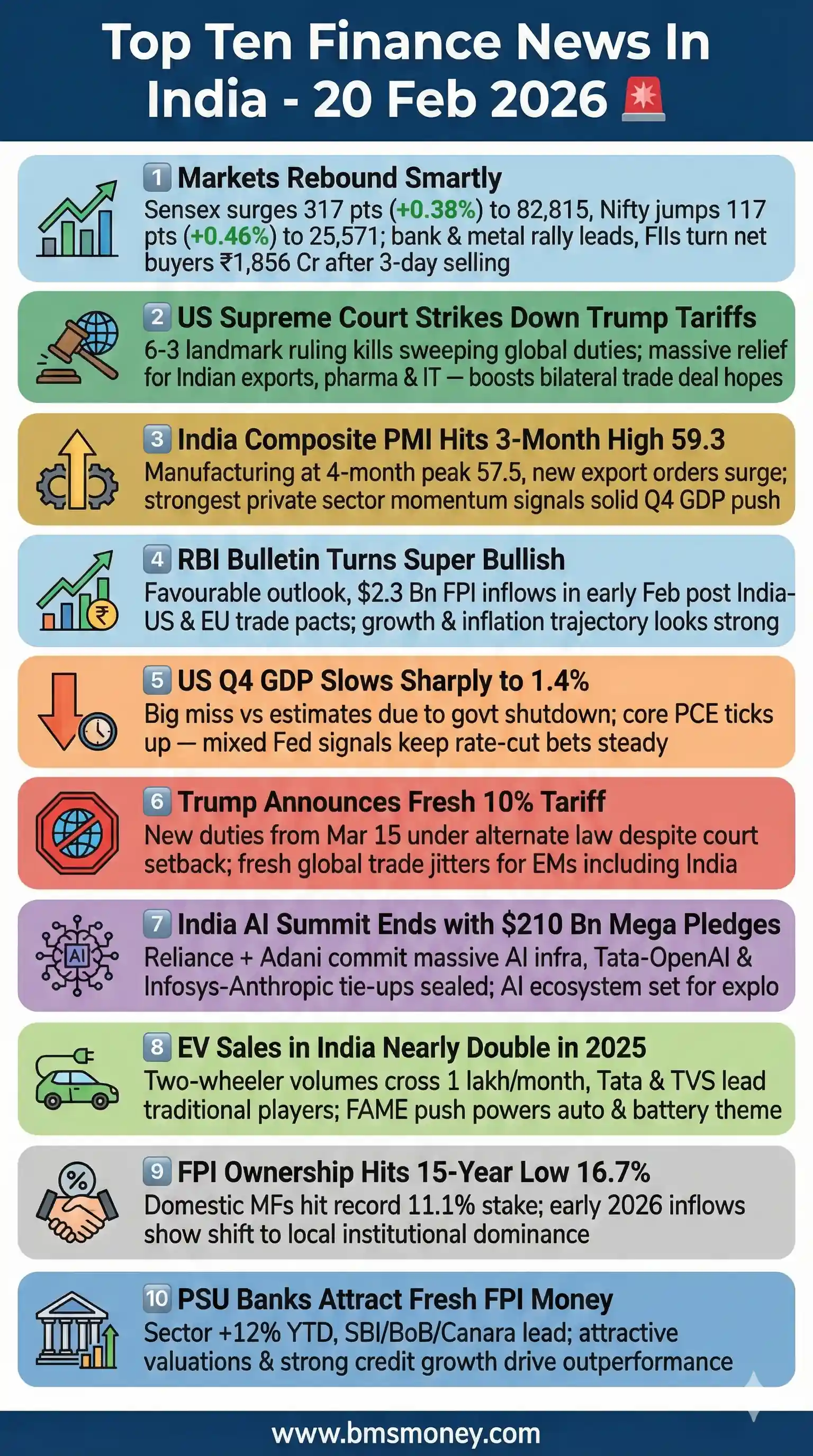

Sensex Rises 317 Points, Nifty Closes Above 25,550 on Bank-Led Rally

Indian benchmark indices staged a smart recovery on February 20 after the previous session’s 1.2% decline, as strong buying emerged in banking, metals, power and FMCG counters. The BSE Sensex climbed 316.57 points or 0.38% to close at 82,814.71, while the NSE Nifty advanced 116.90 points or 0.46% to settle at 25,571.25. Market breadth was positive with 36 of the 50 Nifty constituents finishing in the green and the advance-decline ratio standing at a healthy 2.1:1.

Banking stocks led the charge with HDFC Bank rising 1.8%, ICICI Bank 1.5% and State Bank of India gaining 1.2% on expectations of steady credit growth and improving asset quality. Metals pack surged on global cues with Hindalco up 3.2% and Tata Steel 2.1%. Power and infrastructure names such as NTPC and Larsen & Toubro added between 1.5% and 2.8%. In contrast, IT stocks remained under pressure with TCS and Infosys declining 0.7-0.9% amid global tech sector rotation.

Turnover on NSE rose 12% to ₹1.28 lakh crore, indicating fresh participation. Foreign institutional investors turned net buyers to the tune of ₹1,856 crore after three straight days of selling, while domestic institutions continued their consistent buying at ₹2,341 crore. The recovery has lifted the Nifty above its immediate support of 25,400 and opened the possibility of a move towards 25,800-26,000 in the coming sessions provided global cues remain stable. Analysts believe the day’s action reflects resilient domestic liquidity and bargain hunting after the recent correction.

US Supreme Court Strikes Down President Trump’s Global Tariffs

In a landmark 6-3 ruling, the US Supreme Court held that President Trump overstepped his constitutional authority by imposing sweeping global tariffs under the International Emergency Economic Powers Act without explicit Congressional approval. The decision invalidates tariffs ranging from 10% to 60% that had been levied on imports from over 40 countries since January 2025.

US equity markets reacted positively with the S&P 500 rising 0.72% and Nasdaq gaining 1.1% in afternoon trade. The dollar index fell 0.4% while 10-year Treasury yields eased four basis points. The ruling removes a major overhang on global trade and is particularly beneficial for export-dependent economies. For India, the verdict strengthens the recently signed interim trade agreement and reduces the risk of retaliatory duties on key sectors such as pharmaceuticals, textiles, gems & jewellery and engineering goods.

Indian exporters and IT services firms with significant US exposure are expected to see improved order visibility. Trade ministry officials in New Delhi welcomed the judgment, stating it paves the way for smoother finalisation of the full bilateral trade pact. Market participants believe the development could support fresh FPI inflows into Indian equities over the next few weeks.

Reuters: https://www.reuters.com/business/us-stock-futures-muted-ahead-economic-data-2026-02-20/

India’s Composite PMI Rises to Three-Month High of 59.3 in February

HSBC and S&P Global’s flash PMI survey released on February 20 showed India’s private sector activity expanding at the fastest pace in three months. The composite output index climbed to 59.3 in February from 58.4 in January, comfortably above the 50-point expansion threshold. Manufacturing PMI rose sharply to a four-month high of 57.5 while services PMI remained robust at 58.4.

New business inflows accelerated in both sectors, with new export orders in services recording the strongest growth since August 2025. Backlogs of work increased for the sixth straight month, signalling capacity constraints. Input cost inflation touched a 15-month high, driven by higher raw material and wage pressures, yet firms maintained pricing power and business confidence reached its highest level in 12 months.

Economists at Nomura and Goldman Sachs described the print as “broad-based and encouraging”, reinforcing expectations of 6.8-7.0% GDP growth in Q4 FY26. The data is likely to keep RBI’s policy bias neutral in the April review and supports continued foreign investor interest in India’s growth story. Bond yields eased 2-3 basis points while the rupee strengthened marginally to 86.72 against the dollar.

RBI Bulletin Highlights Favourable Outlook and FPI Revival After Trade Pacts

The Reserve Bank of India’s monthly bulletin for February noted that the near-term economic outlook remains “clearly favourable” with multiple growth drivers firing simultaneously. Benign inflation trajectory, steady fiscal consolidation, healthy rural demand and the positive impact of recent trade agreements with the EU and the US were cited as key positives.

Net foreign portfolio investment into equity and debt segments touched $2.3 billion in the first 15 days of February, reversing the heavy outflows seen in 2025. The RBI also highlighted that the interim India-US trade deal and the India-EU FTA would enhance market access, improve export competitiveness and help integrate Indian manufacturing into global value chains.

The central bank maintained its projection of 6.5% GDP growth for FY26 and flagged that headline CPI is likely to average 4.2% in the second half of the year. Analysts believe the commentary will encourage long-only investors and could support a further 150-200 basis point compression in India’s country risk premium over the next quarter.

Business Standard: https://www.business-standard.com/economy/news/near-term-outlook-favourable-to-sustain-high-growth-momentum-rbi-126022001193_1.html

US Q4 GDP Growth Slows to 1.4% Amid Government Shutdown Impact

The US Bureau of Economic Analysis reported that real GDP grew at an annualised rate of just 1.4% in the fourth quarter of 2025, significantly below the 2.8% consensus estimate and the third-quarter’s 3.1% pace. Government shutdown-related disruptions, weaker consumer spending and inventory drawdown were the primary drags. Full-year 2025 GDP growth stood at 2.2%.

Core PCE inflation for December came in at 2.8% year-on-year, up from 2.6% in November. Atlanta Fed President Raphael Bostic remarked that while the annual number remains respectable, policymakers must remain vigilant on underlying price pressures. Markets interpreted the data as mixed, keeping the probability of a March Fed rate cut at around 35%.

For India, the softer US growth number initially weighed on IT and pharma stocks but the Supreme Court tariff ruling later in the day more than offset the negative sentiment. Indian ADRs on NYSE closed mixed with mixed signals for the next trading session.

Reuters: https://www.reuters.com/world/us/us-economic-growth-slows-sharply-fourth-quarter-2026-02-20/

President Trump Announces 10% Tariff Under Alternative Authority

Hours after the Supreme Court struck down the earlier tariff regime, President Trump addressed the media and confirmed that a 10% across-the-board tariff on all imports would be imposed using alternative legal provisions under the Trade Expansion Act of 1962. The new tariffs are scheduled to take effect from March 15, 2026, giving trading partners a short window to negotiate.

The announcement trimmed some of the earlier market gains but did not trigger a sell-off. US futures remained in positive territory. Indian officials indicated that the interim trade deal already provides India with a lower effective rate on several product lines and further talks would be accelerated. Sectors such as automobiles, chemicals and steel could face marginal pressure while pharmaceuticals and IT services remain largely insulated.

Market participants expect heightened volatility in the run-up to March 15 but believe the overall impact on India will be limited given the diversified nature of its export basket and the ongoing bilateral negotiations.

The Wall Street Journal: https://www.wsj.com/livecoverage/stock-market-today-us-gdp-report-02-20-26

India AI Impact Summit 2026 Concludes with Major Partnerships and Investment Pledges

The five-day India AI Impact Summit concluded in New Delhi on February 20 with landmark announcements worth over $210 billion in committed investments. Reliance Industries and Adani Group together pledged $210 billion over the next five years towards domestic AI compute infrastructure, data centres and semiconductor fabrication. Tata Group formalised a strategic partnership with OpenAI while Infosys signed a multi-year collaboration with Anthropic.

Google CEO Sundar Pichai delivered the valedictory keynote and announced expansion of Google’s AI research lab in Bengaluru. The US delegation, led by Commerce Secretary, promoted “sovereign AI” exports and highlighted India as the preferred partner for responsible AI development. Over 40 MoUs were signed covering talent skilling, ethical AI frameworks and public-sector adoption.

The outcomes are expected to create significant revenue opportunities for listed companies in technology, infrastructure, power and capital goods sectors. Brokerages have upgraded earnings estimates for Tata Consultancy Services, Infosys, HCL Tech and Larsen & Toubro by 8-12% for FY27-28. The summit has clearly positioned India as an emerging global AI powerhouse.

Electric Vehicle Sales in India Nearly Double in 2025, Traditional Players Lead

Provisional industry data released on February 20 revealed that passenger electric vehicle and two-wheeler sales in calendar 2025 nearly doubled from 2024 levels. Two-wheeler EV monthly volumes consistently crossed 100,000 units from September onwards, while passenger EV registrations grew 92% year-on-year.

Traditional two-wheeler majors such as TVS Motor, Hero MotoCorp and Bajaj Auto collectively captured 68% market share, overtaking newer pure-play EV companies. In the four-wheeler segment, Tata Motors retained leadership with 62% share while MG Motor and Mahindra also gained ground. Continued FAME-II incentives, state-level subsidies and improving charging infrastructure were key growth drivers.

Analysts at JM Financial and Motilal Oswal have raised FY27 volume estimates for the auto ancillary and battery ecosystem by 15-18%. The trend is expected to sustain into 2026 with new model launches and further policy support, making the entire auto value chain an attractive long-term investment theme.

FPI Ownership in NSE-Listed Firms Falls to 15-Year Low of 16.7%

Latest shareholding pattern data for the December 2025 quarter showed foreign portfolio investors’ aggregate stake in NSE-listed companies declining to 16.7% — the lowest level since 2010. This followed record net outflows of $18.9 billion during calendar 2025 amid global rate hikes and domestic election-related uncertainty.

Simultaneously, domestic mutual funds increased their ownership to a record 11.1%, reflecting strong retail and systematic investment plan flows. Early February 2026 has witnessed a sharp reversal with net FPI inflows of over $3.1 billion on the back of trade-deal optimism and robust macro data.

The shift towards greater domestic institutional ownership is viewed as structurally positive for market stability. Brokerages note that lower FPI concentration reduces the risk of sudden sell-offs during global risk-off episodes while domestic institutions provide consistent demand at every dip.

PSU Banks Draw Fresh FPI Interest, Driving Sectoral Outperformance

Foreign portfolio investors selectively increased stakes in public-sector banks during the first half of February, drawn by attractive valuations, improving return on equity and sustained credit growth. The Nifty PSU Bank index has gained 12% year-to-date, comfortably outperforming the broader Nifty’s 4.8% rise.

Key beneficiaries included State Bank of India, Bank of Baroda, Canara Bank and Punjab National Bank, where FPI ownership rose between 40 and 110 basis points. Strong Q3 earnings, lower slippages and government’s continued capital infusion have restored investor confidence.

The sectoral outperformance contributed nearly 35 basis points to the Nifty’s gain on February 20. With PSU banks trading at 0.9-1.1 times book value against private banks at 2.2-2.8 times, analysts see further re-rating potential of 15-20% over the next 12 months, especially if credit growth remains above 12% and asset quality stays stable.

Note: This briefing is based on verified public sources available as of February 21, 2026 morning. Markets remain sensitive to evolving geopolitical developments, US tariff implementation timeline and the upcoming corporate earnings season.