-

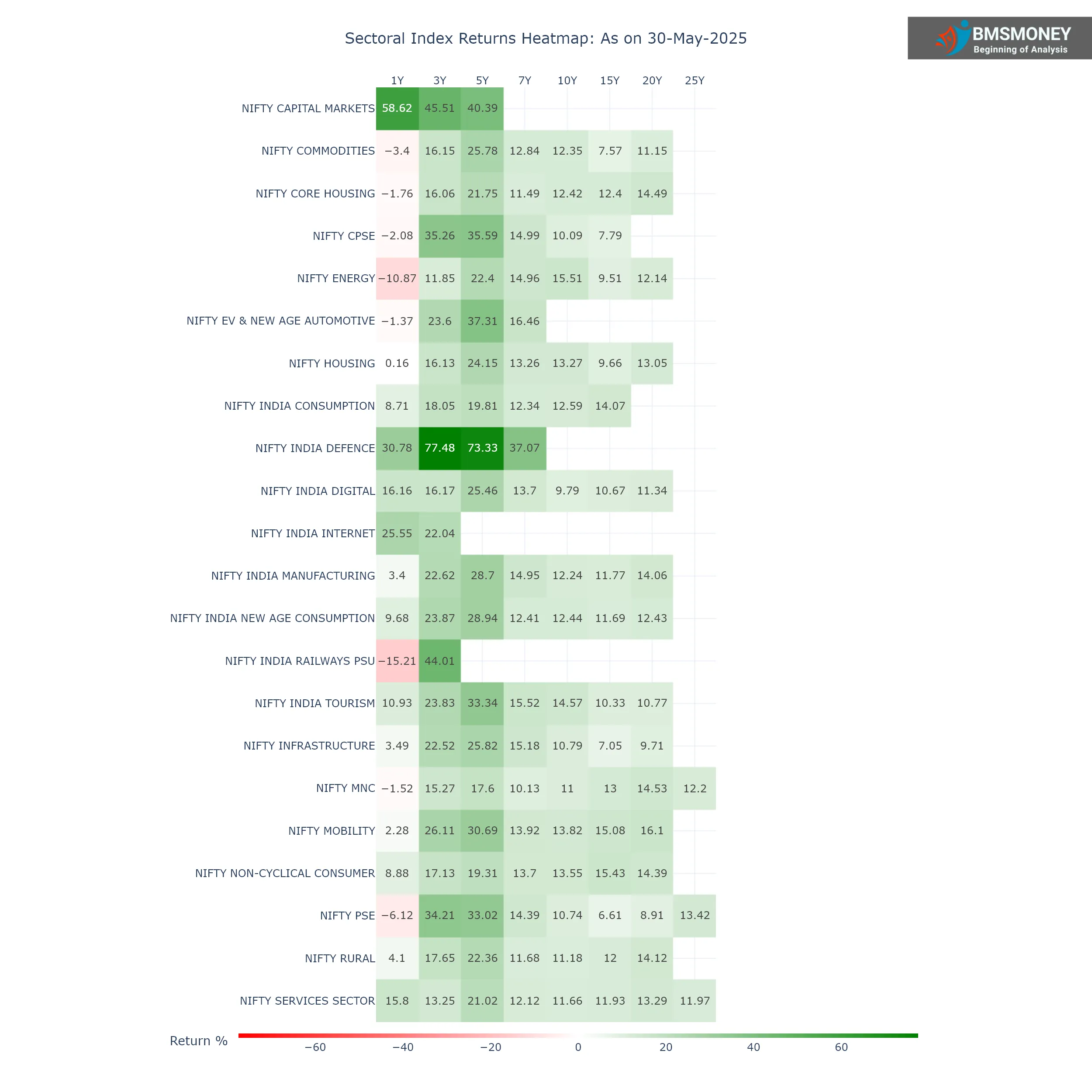

Defence Dominates: NIFTY INDIA DEFENCE delivered extraordinary returns (77.48% 3Y CAGR), driven by government focus and strong order books.

-

EV & Capital Markets Shine: NIFTY EV & NEW AGE AUTOMOTIVE and NIFTY CAPITAL MARKETS show robust multi-year growth (37%+ 5Y CAGR), capturing key structural shifts.

-

Steady Compounders Hold Strong: Manufacturing, Consumption, Tourism, and Infrastructure indices demonstrate consistent, healthy long-term returns (12-15%+ 10Y CAGR).

-

Time Horizon is Critical: Dramatic short-term swings smooth out significantly; true wealth creation stems from sustained multi-year compounding.

As the Indian equity market continues its dynamic evolution, thematic investing has surged in popularity, offering investors targeted exposure to specific growth narratives and structural shifts within the broader economy. The National Stock Exchange (NSE) provides a comprehensive suite of thematic indices, tracking sectors ranging from digital transformation and defence to infrastructure and consumption. Performance data as of May 30th, 2025, reveals fascinating trends, highlighting both runaway successes and sectors facing headwinds, offering crucial insights for portfolio construction. Let's dissect the returns across various time horizons to understand which themes are delivering and the critical importance of investment horizons.

The Standout Stars: Defence and New Age Mobility Lead the Charge

Without question, the NIFTY INDIA DEFENCE index is the undisputed champion. Its performance is nothing short of spectacular:

-

1-Year: +30.78%

-

3-Year CAGR: +77.48% (Astronomical compounding)

-

5-Year CAGR: +73.33%

-

7-Year CAGR: +37.07%

This dominance reflects the massive government push for indigenous defence manufacturing, significant order inflows for both public and private sector players, and heightened geopolitical tensions driving global and domestic demand. Defence has transitioned from a niche PSU play to a high-growth, multi-company thematic powerhouse.

Close on its heels is the NIFTY EV & NEW AGE AUTOMOTIVE index, capturing the electric vehicle revolution and associated ecosystem:

-

1-Year: -1.37% (Recent consolidation)

-

3-Year CAGR: +23.60%

-

5-Year CAGR: +37.31%

-

7-Year CAGR: +16.46%

Despite a slight pullback over the last year, the sustained high growth over 3, 5, and 7 years underscores the secular shift towards electrification, shared mobility, and advanced automotive technologies. Policy support (FAME schemes, PLI) and rapidly evolving consumer preferences continue to fuel this theme.

Capital Markets: A High-Growth Niche

The NIFTY CAPITAL MARKETS index, representing brokers, asset management companies, and exchanges, has delivered exceptional returns, albeit with a shorter track record:

-

1-Year: +58.62% (Highest 1-year return)

-

3-Year CAGR: +45.51%

-

5-Year CAGR: +40.39%

This stellar performance is driven by India's deepening financial markets, surging retail participation (Demat accounts), robust IPO activity, and sustained growth in Assets Under Management (AUM) for mutual funds. It capitalizes directly on the financialization of savings.

The Steady Compounders: Consumption, Manufacturing, and Infrastructure Resurface

Several themes demonstrate the power of consistent, albeit less explosive, growth over longer periods:

-

NIFTY INDIA MANUFACTURING (3Y: 22.62%, 5Y: 28.70%, 7Y: 14.95%, 10Y: 12.24%): The "Make in India" push, PLI schemes, China+1 diversification, and improving global demand are revitalizing this core sector. Returns are robust across all reported horizons.

-

NIFTY INDIA TOURISM (3Y: 23.83%, 5Y: 33.34%, 7Y: 15.52%, 10Y: 14.57%): Pent-up post-pandemic demand, rising disposable incomes, improved infrastructure (airports, highways), and government focus are driving airlines, hotels, and travel services.

-

NIFTY INDIA NEW AGE CONSUMPTION (3Y: 23.87%, 5Y: 28.94%, 7Y: 12.41%, 10Y: 12.44%) & NIFTY INDIA CONSUMPTION (3Y: 18.05%, 5Y: 19.81%, 7Y: 12.34%, 10Y: 12.59%): India's core consumption story remains resilient, evolving to include digital-first brands (New Age) alongside traditional FMCG and retail giants. Rising per capita income and aspirational spending underpin this theme.

-

NIFTY INFRASTRUCTURE (3Y: 22.52%, 5Y: 25.82%, 7Y: 15.18%, 10Y: 10.79%) & NIFTY MOBILITY (3Y: 26.11%, 5Y: 30.69%, 7Y: 13.92%, 10Y: 13.82%): Massive government capex on roads, railways, ports, and urban infrastructure, coupled with recovery in the auto sector (Mobility), is driving these indices. The focus on logistics efficiency and connectivity is key.

-

NIFTY NON-CYCLICAL CONSUMER (3Y: 17.13%, 5Y: 19.31%, 7Y: 13.70%, 10Y: 13.55%, 15Y: 15.43%): This index, likely heavy on staples and essential services, showcases remarkable consistency across all timeframes, highlighting the defensive nature of essential consumption.

Top Performing Funds for You

Top Performing Equity Funds Top Performing Debt Funds Top Performing Hybrid FundsPSU Powerhouses: High Growth with Recent Stumbles

The NIFTY CPSE and NIFTY PSE indices, representing Central Public Sector Enterprises, delivered phenomenal 3 and 5-year returns (CPSE: 35.26%, 35.59%; PSE: 34.21%, 33.02%), benefiting from government focus on divestment, improved efficiencies, and sector-specific tailwinds (especially energy). However, recent 1-year returns (-2.08% and -6.12% respectively) indicate potential profit-taking, valuation concerns, or sector-specific challenges (e.g., energy price volatility). Their longer-term 10-year CAGRs (CPSE: 10.09%, PSE: 10.74%) show the significant acceleration more recently. NIFTY INDIA RAILWAYS PSU (-15.21% 1Y, +44.01% 3Y) exemplifies this volatility – massive gains followed by a sharp correction.

The Digital & Internet Dichotomy

The technology theme shows interesting nuances:

-

NIFTY INDIA DIGITAL (3Y: 16.17%, 5Y: 25.46%, 7Y: 13.70%, 10Y: 9.79%): Delivers solid, consistent growth across all longer horizons, reflecting the broad-based digitization of Indian businesses and services (IT services, fintech, enterprise software).

-

NIFTY INDIA INTERNET (1Y: 25.55%, 3Y: 22.04%): Shows stronger recent momentum but lacks longer-term data. This likely captures more consumer-facing internet platforms (e-commerce, food delivery, travel aggregators), which experienced significant volatility post-pandemic highs but seem to be regaining traction.

Facing Headwinds: Commodities, Energy, and Core Housing

A few themes struggled over the past year:

-

NIFTY COMMODITIES (-3.40% 1Y): Global commodity price fluctuations and cooling demand likely impacted this sector, despite strong 3Y and 5Y CAGRs.

-

NIFTY ENERGY (-10.87% 1Y): The most significant 1-year decline. Volatility in global crude oil and gas prices, potential regulatory changes, and the transition pressure on traditional energy players are key factors. Longer-term returns remain healthy (3Y: 11.85%, 5Y: 22.40%, 7Y: 14.96%, 10Y: 15.51%), showing its historical strength.

-

NIFTY CORE HOUSING (-1.76% 1Y) & NIFTY HOUSING (+0.16% 1Y): Higher interest rates impacting mortgage affordability and a potential slowdown in real estate sales after a strong run appear to be moderating growth in the housing finance sector, though longer-term numbers (e.g., Housing 5Y: 24.15%) remain strong.

Top Performing Equity Fund Categories for You

Top Performing Large Cap Funds Top Performing Mid Cap Funds Top Performing Small Cap FundsThe Enduring Lesson: Time Horizon is Paramount

The analysis powerfully reinforces the most fundamental principle of equity investing: Time in the market trumps timing the market. Consider:

-

Smoothing Volatility: The dramatic 1-year swings (e.g., Defence +30.78% vs. Energy -10.87%, Railways PSU -15.21%) largely smooth out over 3, 5, 7, and 10-year horizons. Short-term noise gives way to underlying growth trends.

-

Power of Compounding: The most impressive wealth creation (e.g., Defence, EV, Capital Markets) comes from sustained high growth over multiple years (3Y, 5Y CAGR). Compounding turns consistent performance into exponential gains.

-

Identifying Structural Winners: While short-term laggards exist, themes with strong long-term CAGRs (Manufacturing, Consumption, Digital, Infrastructure, Tourism, Non-Cyclical Consumer) demonstrate resilience and the ability to navigate cycles. These represent structural shifts in the Indian economy.

-

New Themes Need Time: Spectacular short-term returns in newer themes (e.g., Defence, Internet, Railways PSU) are exciting but lack the long-term track record of more established sectors. Their sustainability remains to be proven across full market cycles.

-

Diversification Across Time and Theme: No single theme leads perpetually. Diversification across complementary themes with different growth drivers and risk profiles (e.g., combining high-growth Defence/EV with steady Consumption/Digital) and maintaining a sufficiently long investment horizon is the optimal strategy to manage risk and capture India's multifaceted growth story.

Top Performing Debt Fund Categories for You

Top Performing Liquid Funds Top Performing Ultra Short Duration Funds Top Performing Corporate Bond FundsConclusion: A Tapestry of Growth

The NSE thematic index performance as of May 2025 paints a vibrant picture of India's economic transformation. High-flying sectors like Defence and New Age Automotive showcase cutting-edge growth drivers, while Manufacturing, Consumption, and Infrastructure reaffirm their status as core engines of the economy. The resurgence of PSUs, despite recent stumbles, highlights evolving narratives. Simultaneously, the data underscores the challenges in commodities and traditional energy and the sensitivity of housing to interest rates.

For investors, the key takeaways are clear:

-

Thematic investing offers potent exposure to specific growth vectors within the Indian juggernaut.

-

Vigilant research is crucial: Understand the drivers, valuations, and risks inherent in each theme.

-

Embrace volatility with a long lens: Short-term fluctuations are inevitable; focus on the multi-year trajectory.

-

Prioritize the long term: True wealth creation in equities is a marathon, powered by compounding, not a sprint.

-

Diversify strategically: Spread allocations across themes with different risk-return profiles and economic sensitivities.

India's growth story is being written across multiple sectors simultaneously. The NSE thematic indices provide the lenses to focus on each compelling chapter. By aligning investments with these powerful trends and maintaining the discipline of a long-term perspective, investors stand poised to participate meaningfully in the next phase of India's remarkable economic journey. The data as of May 2025 is not just a snapshot of the past; it's a roadmap, highlighting both the exhilarating peaks and the enduring pathways to sustainable growth.