Indian equity markets are set for a positive opening on January 23, 2026, extending a relief rally fueled by easing global tensions and domestic buying in key sectors, despite ongoing FII outflows.

-

Opening Signal: GIFT Nifty indicates a strong, optimistic start, up approximately 0.87%.

-

Market Driver: A relief rally continues as global trade tensions show signs of easing.

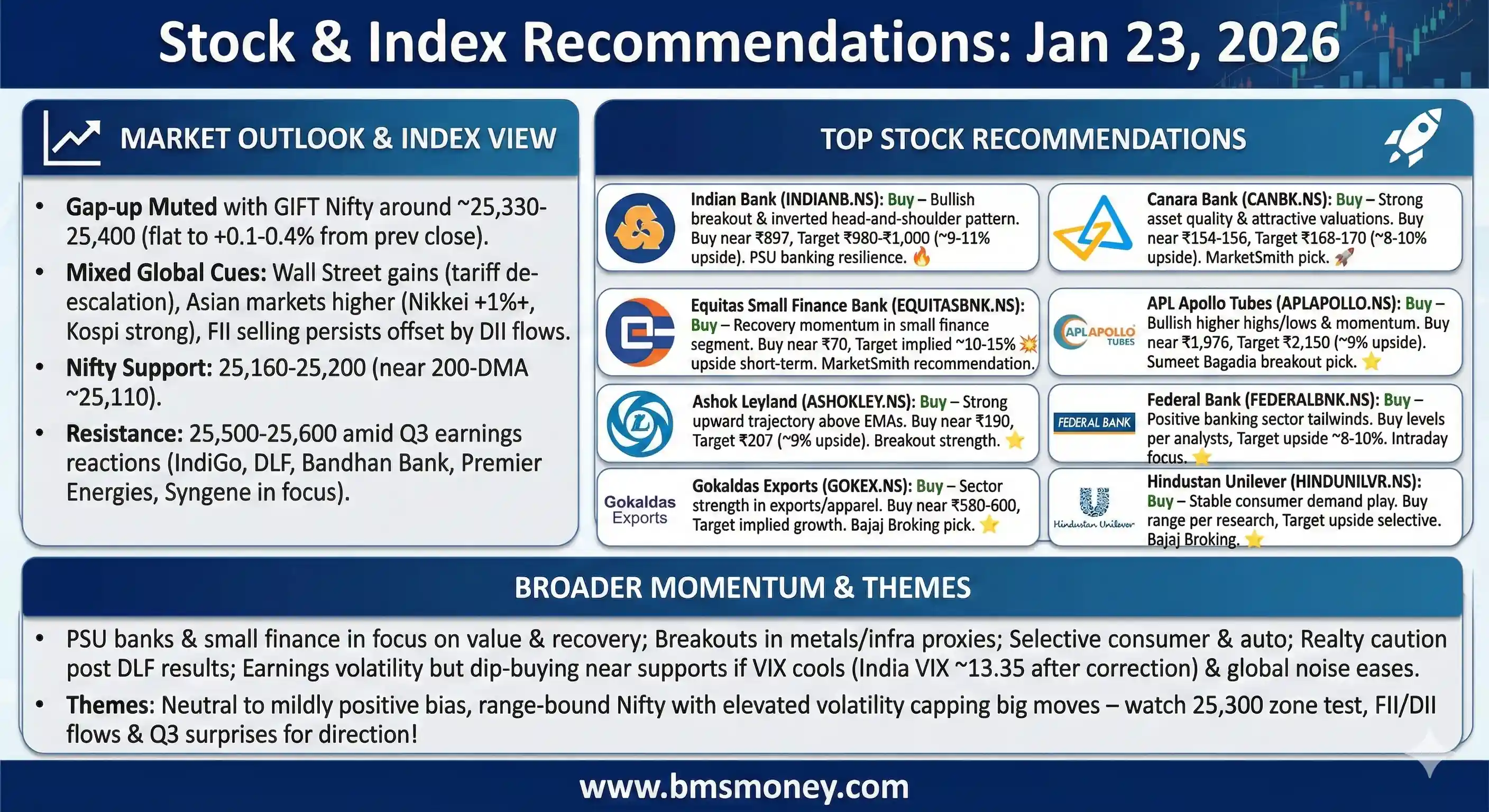

The Indian equity markets are poised for a positive start on January 23, 2026, following a relief rally in the previous session amid easing global trade tensions. The GIFT Nifty futures were trading around 25,381, up approximately 0.87%, signaling an optimistic opening for the benchmark indices. Overnight cues from global markets were supportive, with European indices like the DAX and STOXX 50 posting strong gains, while US futures remained steady. Domestically, the Nifty 50 closed 0.53% higher at 25,289.90, and the Sensex rose 0.49% to 82,307.37, driven by buying in banking and IT sectors. Volatility eased with the India VIX dropping, but foreign institutional investors (FIIs) continued net selling of around ₹2,549 crore, offset by domestic institutional investors (DIIs) purchasing ₹4,222 crore.

Today's themes include a focus on the banking sector amid improving asset quality and credit growth, alongside selective picks in consumer goods and automobiles. A total of around 20-25 unique recommendations were aggregated from credible sources like brokerages and financial portals, with a bias toward 'Buy' calls on undervalued large-caps. Standout calls include MarketSmith India's upgrade of Canara Bank to 'Buy', ICICI Direct's 'Buy' on Hyundai Motor India with a 27% upside, and Hindu BusinessLine's 'Buy' on Indian Bank targeting ₹980-₹1,000. Investors should monitor Q3 earnings from key players like JSW Steel and ongoing geopolitical developments.

Section 1: Index Outlook

The near-term outlook for major indices remains cautious but with a positive bias, supported by technical rebounds and global de-escalation. Analysts expect range-bound trading with volatility, as the Nifty needs a decisive close above 25,850 to confirm an uptrend. Immediate support is seen at 25,160-25,130 (near 200-DMA), while resistance lies at 25,500-25,600. Bank Nifty shows strength, potentially leading sectoral gains.

| Index | Recommendation | Target/Range | Key Driver | Source |

|---|---|---|---|---|

| Nifty 50 | Bullish | 25,500-25,850 | Relief rally on global cues, banking strength | Moneycontrol, CNBC-TV18 |

| Sensex | Positive Bias | 82,500-83,000 | DII buying offsetting FII outflows, technical support | ET Now, Hindu BusinessLine |

| Bank Nifty | Bullish | 59,500-60,000 | Improved asset quality, credit growth in PSUs | PL Capital, Money Bells |

Section 2: Sector-Wise Stock Picks

Recommendations today lean toward banking and financials, with selective buys in automobiles, consumer goods, and industrials. Brokerages like ICICI Direct and MarketSmith India emphasized value in mid-to-large caps, citing attractive valuations post-corrections. No major 'Sell' calls were noted except for isolated ones like GAIL. Upside potentials range from 12-27%, with rationales tied to earnings recovery and sector tailwinds. A bar chart of target upsides (based on current prices) highlights banking's prominence:

- Banking & Financials: Highest upsides (avg. 20%)

- Automobiles: Moderate (avg. 15-25%)

- Consumer Goods: Selective recovery plays (10-20%)

Banking & Financials

- Canara Bank (CANBK.NS) – Buy, Target: ₹170 (Upside: ~10%), Rationale: Strong Q3 performance with improved NIMs and asset quality; attractive valuations amid PSU bank rally. Source: MarketSmith India.

- Indian Bank (INBK.NS) – Buy, Target: ₹980-₹1,000 (Upside: ~9-11%), Rationale: Surge confirms inverted head-and-shoulder pattern; bullish short-term outlook with robust earnings. Source: Hindu BusinessLine.

- Equitas Small Finance Bank (EQSF.NS) – Buy, Target: ₹85 (Upside: ~21%), Rationale: Recovery in small finance segment with healthy loan growth. Source: MarketSmith India.

- HDFC Bank (HDFC.NS) – Buy, Target: ₹2,000 (Upside: ~15%), Rationale: Upgraded amid attractive valuations and expected credit growth; part of Axis top picks. Source: Axis Securities.

- HDFC Life Insurance (HDFCLIFE.NS) – Buy, Target: ₹800 (Upside: 25%), Rationale: Strong premium growth and margin expansion. Source: ICICI Direct.

- HDFC AMC (HDFCAMC.NS) – Buy, Target: ₹5,100 (Upside: 26%), Rationale: AUM growth and favorable equity market trends. Source: ICICI Direct.

IT & Tech

- Limited fresh calls today; general hold on large-caps like TCS and HCL Tech amid Q3 results focus. No specific targets issued on January 23.

Automobiles & Industrials

- Hyundai Motor India (HYUNDAI.NS) – Buy, Target: ₹2,070 (Upside: 27%), Rationale: Robust sales volume and EV push; positive industry outlook. Source: ICICI Direct.

- Aeroflex Industries (AERO.NS) – Buy, Target: ₹280 (Upside: 26%), Rationale: Export growth and margin improvement. Source: ICICI Direct.

Consumer Goods

- Godrej Consumer Products (GODREJCP.NS) – Buy, Target: ₹1,350 (Upside: ~10%), Rationale: Recovery at breakout levels; elevated bounce potential. Source: Times of India.

- Swiggy (SWIGGY.NS) – Buy, Target: ₹361 (Upside: ~8%), Rationale: Post-bearish flag recovery; strong consumer demand. Source: Times of India.

Others

- GAIL (GAIL.NS) – Sell, Target: ₹150 (Downside: ~8%), Rationale: Closing low amid selling pressure; retest of March 2025 lows likely. Source: Times of India.

Section 3: Global & Thematic Insights

Global brokerages like Elara Capital maintained 'Accumulate' on Havells India (target ₹1,620, upside 12%), citing consumer durables recovery. Axis Securities highlighted thematic plays in BFSI and consumption, overweight on SBI and Bajaj Finance for midcap value. No major regulatory updates from BSE/NSE today, but block deals in stocks like IndiGo imply institutional interest. Macquarie sees value in Indian midcaps amid cross-border flows, though tariff overhangs persist for exports.

Conclusion & Disclaimer

Overall market sentiment is neutral to bullish, with banking leading potential upside amid DII support. Investors should watch key levels in Nifty and focus on undervalued PSUs like Indian Bank for short-term gains. This pre-market snapshot may evolve with intraday developments.

This is aggregated data for informational purposes; consult a financial advisor before investing. Not investment advice. Data sourced as of 8:30 AM IST on January 23, 2026.

Sources & Citations

- India Infoline: https://www.indiainfoline.com/news/markets/top-stocks-for-today-23rd-january-2026

- Mint: https://www.livemint.com/market/stock-market-news/stock-recommendations-23-january-marketsmith-india-top-stock-picks-sensex-nifty-11769083101353.html

- Moneycontrol: https://www.moneycontrol.com/news/business/markets/stocks-to-watch-today-indigo-bandhan-bank-premier-energies-syngene-go-digit-dlf-home-first-finance-ashoka-buildcon-rk-swamy-in-focus-on-23-january-13786827.html

- Hindu BusinessLine: https://www.thehindubusinessline.com/multimedia/video/todays-stock-recommendation-january-23-2026/article70537789.ece

- Economic Times: https://m.economictimes.com/markets/stocks/news/stocks-to-buy-in-2026-havells-india-jk-cement-among-5-stocks-that-could-give-double-digit-return-in-long-term/brokerage-recommendations/slideshow/126919730.cms

- ICICI Direct: https://www.icicidirect.com/ (browsed for specific calls)