Indian markets are set for a muted-to-soft opening on February 23, 2026, as fresh U.S. global tariffs and mixed Asian cues weigh on sentiment. While domestic cyclicals and PSU banks show resilience, early focus remains on corporate developments and selective technical picks amid subdued pre-market analyst activity.

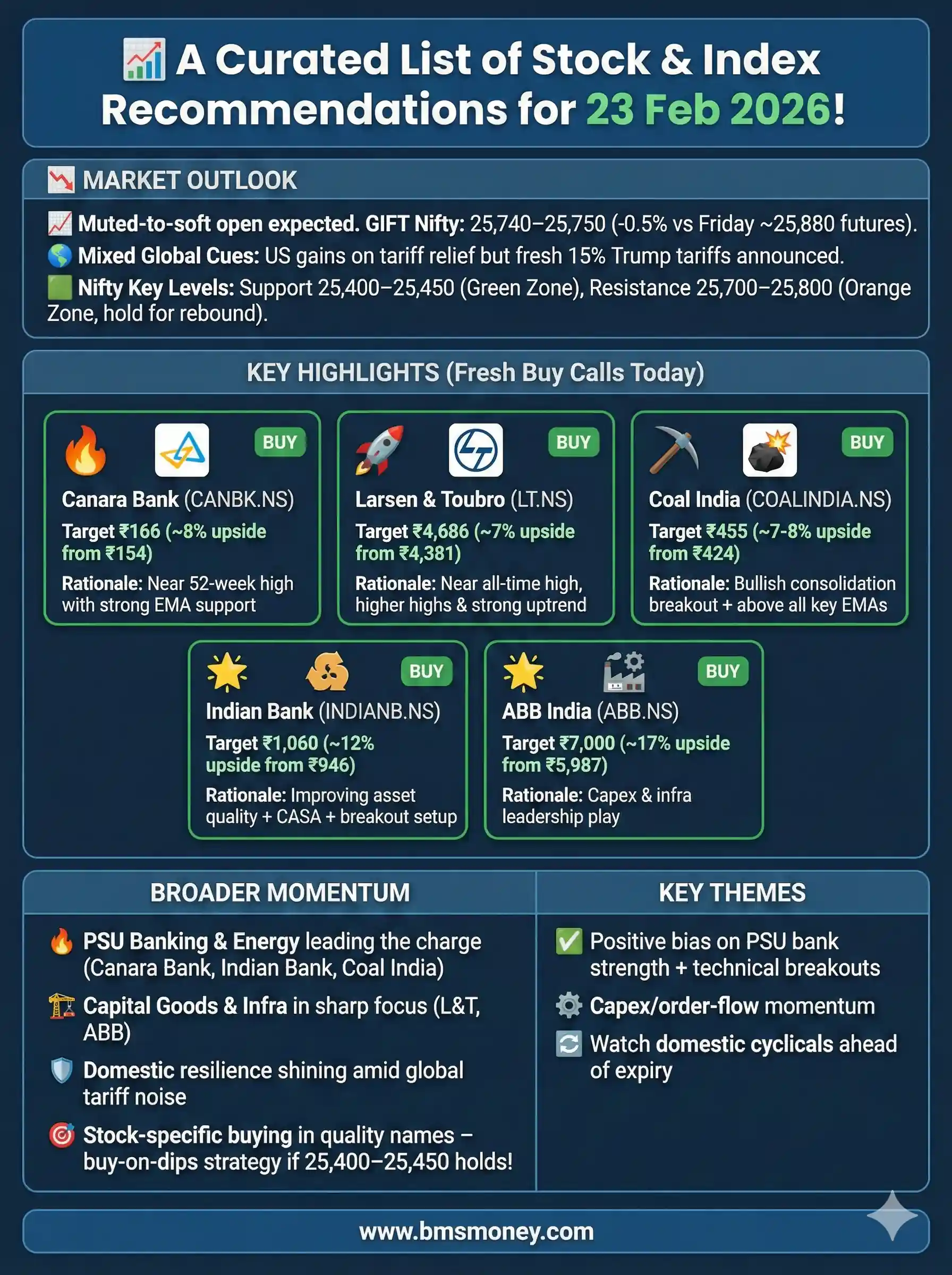

Indian equities are set for a muted-to-soft open on Monday, February 23, 2026, amid mixed global cues and fresh U.S. trade policy developments. GIFT Nifty traded in a narrow range around 25,730–25,750 levels in early morning deals (approximately 0.5% lower to flat versus Friday’s Nifty futures close), pointing to a flat-to-mildly negative start for the benchmark indices.

Overnight, U.S. markets closed higher after the Supreme Court struck down broad “reciprocal” tariffs, but President Trump responded with a new executive order imposing a 15% global tariff on imports effective February 24, raising concerns for export-sensitive sectors. Asian markets opened mixed-to-positive, with limited follow-through. Domestically, focus remains on Q3 earnings digestion, corporate actions, and resilience in domestic cyclicals.

Only a handful of fresh analyst-driven calls emerged in pre-market hours, reflecting the early timing of the snapshot (pre-8:30 AM IST). Key themes include PSU banks (strong technical setups), infrastructure/capital goods (order momentum and capex play), and energy (defensive positioning). Stocks-to-watch lists are dominated by corporate events such as UPL’s restructuring, Cipla’s USFDA update, Vikram Solar’s cell supply deal, RailTel’s order win, and IDFC First Bank’s fraud disclosure.

Standout calls: Choice Broking’s Buy on Coal India, L&T, and Canara Bank; MarketSmith India’s Buys on Indian Bank and ABB India. Overall, 8–10 actionable ideas surfaced across technical and fundamental desks.

Section 1: Index Outlook Nifty 50 closed Friday at 25,571.25 (+0.46%), forming a small bullish candle while holding above the 200-DMA. Sensex ended at 82,814.71 (+0.38%). Bank Nifty closed at ~61,172 (+0.71%).

Analysts expect consolidation with a slight positive bias in the near term, provided key supports hold. Global tariff noise may cap upside, but domestic institutional buying and select earnings beats provide a floor.

| Index | Recommendation | Target/Range | Key Driver | Source |

|---|---|---|---|---|

| Nifty 50 | Sideways-to-Positive | 25,400–25,900 (break >25,888 for fresh uptrend) | Support at 25,400–25,450; resistance 25,700–25,750 | Choice Broking (Sumeet Bagadia) |

| Sensex | Neutral | 82,500–83,500 | Broad-based buying in Financials/Metals/FMCG | MarketSmith India |

| Bank Nifty | Mildly Bullish | 60,800–61,500+ | Holding above 61,000 psychological level | Choice Broking |

Section 2: Sector-Wise Stock Picks

Banking & Financials (strongest technical cluster today)

- Canara Bank (CANBK.NS) – Buy, Target ₹166, Stop Loss ₹148 (Choice Broking). Trading near 52-week high with support at 100-DMA/20-50 EMA cluster (~₹148). Bullish momentum intact.

- Indian Bank (INDIANB.NS) – Buy in ₹940–960, Target ₹1,060 (2–3 months), Stop Loss ₹890 (MarketSmith India). Improving asset quality, strong CASA, healthy credit growth, RoA expansion; trendline breakout above 100-DMA.

- IDFC First Bank (IDFCFIRSTB.NS) – Stocks-to-watch (event-driven). ₹590 crore fraud disclosure at Chandigarh branch; forensic audit by KPMG underway. Monitor for volatility and any regulatory updates.

Infrastructure & Capital Goods

- Larsen & Toubro (LT.NS) – Buy, Target ₹4,686, Stop Loss ₹4,190 (Choice Broking). Near all-time high, higher highs/higher lows, trading above all key EMAs with upward slope.

- ABB India (ABB.NS) – Buy in ₹5,800–6,000, Target ₹7,000 (2–3 months) (MarketSmith India). Leadership in automation, robotics, energy efficiency; tight-range breakout amid India capex/infra cycle.

- RailTel Corporation (RAILTEL.NS) – Stocks-to-watch. LoI worth ₹1,136 crore (consortium with Ashoka Buildcon) for Maharashtra government office modernisation.

Energy & PSU

- Coal India (COALINDIA.NS) – Buy, Target ₹455, Stop Loss ₹405 (Choice Broking). Constructive bullish setup post-consolidation; trading above all key EMAs with bounce from 100-DMA support. Defensive play amid global uncertainty.

Agrochemicals & Renewables (event-driven movers)

- UPL (UPL.NS) – Stocks-to-watch. Board approved group reorganisation to create independent listed crop protection platform (UPL Global Sustainable Agri Solutions). Value-unlocking move.

- Vikram Solar – Stocks-to-watch. Strategic 2 GW ALMM-compliant solar cell procurement agreement worth ₹2,000 crore with Jupiter International. Positive for renewable supply chain.

Pharma

- Cipla (CIPLA.NS) – Stocks-to-watch. USFDA OAI classification at Greek partner facility (Lanreotide injection); LIC raised stake to 9.091%. Monitor resolution timeline.

Other Notable Mentions

- Bharti Airtel (BHARTIARTL.NS) – Stocks-to-watch. Launched AI & Cyber Threat Research Centre with Zscaler.

- Highway Infrastructure – Stocks-to-watch. New toll collection and road development contracts in Gujarat/Indore.

Numerical Snapshot of Target Upsides (select calls):

- ABB India: ~17% upside

- Indian Bank: ~11–13% upside

- Coal India: ~12–15% upside (from Friday close)

- L&T: ~8–10% upside

- Canara Bank: ~10–12% upside

Section 3: Global & Thematic Insights Global brokerages remained largely silent on fresh India-specific calls in the pre-open window. Focus shifted to U.S.-China-India trade dynamics following the 15% tariff announcement—export-oriented IT/pharma/auto ancillary names may face near-term pressure, while domestic cyclicals (PSU banks, infra, energy) are preferred.

Regulatory/BSE-NSE angle: No major block deals or analyst-meet announcements filtered for today; Dr. Reddy’s investor meet with Kotak Institutional Equities is scheduled (but non-trading impact). Thematic tailwinds include continued capex push (roads, renewables, power transmission) and PSU bank re-rating on improving fundamentals.

Conclusion & Disclaimer Overall market sentiment is neutral-to-cautiously positive for February 23, with domestic resilience likely to offset global tariff jitters. Investors should watch Nifty’s hold above 25,400–25,450 and strength in PSU banks/infra names. Actionable takeaway: Focus on quality domestic plays with strong technicals and order flows (Coal India, L&T, Indian Bank, ABB India) while monitoring tariff-related volatility in export sectors.

This is a pre-market snapshot aggregated from publicly available sources as of ~7:30 AM IST on February 23, 2026. Markets evolve rapidly—updates may emerge post-open. This report is for informational purposes only and does not constitute investment advice. Consult a certified financial advisor before acting on any recommendation. Past performance is not indicative of future results.

Sources & Citations

1. Choice Broking (Sumeet Bagadia) – Buy Calls on Coal India, L&T, Canara Bank + Nifty Outlook

- Full Article: Buy or sell: Sumeet Bagadia recommends three stocks to buy on Monday — 23 February 2026 (LiveMint | Published ~5–6 hours ago)

2. MarketSmith India – Buy Calls on Indian Bank & ABB India + Index Outlook

- Full Article: Stock recommendations for 23 February from MarketSmith India (LiveMint | Published ~2 hours ago)

3. Moneycontrol – Comprehensive “Stocks to Watch” List (UPL, Cipla, Bharti Airtel, Vikram Solar, RailTel, Highway Infrastructure, IDFC First Bank, etc.)

- Full Article: Stocks to Watch Today: UPL, Cipla, Bharti Airtel, Vikram Solar, RailTel Corporation, Highway Infrastructure, IDFC First Bank in focus on 23 February (Moneycontrol | Published ~7 hours ago)

4. Financial Express – Stocks to Watch + Trump Tariff Impact

- Full Article: Stocks to watch today: Vedanta, Cipla, IDFC First Bank and 8 more stocks – Trump’s 15% tariff, key sectors in focus (Financial Express | Updated ~59 minutes ago)

5. CNBC-TV18 – Stocks to Watch (including IDFC First Bank, Vikram Solar, Bharti Airtel, etc.)

- Full Article: Stocks to Watch for Feb 23: NCC, IDFC First Bank, Vikram Solar, Bharti Airtel and more (CNBC-TV18 | Updated yesterday evening, still relevant for today)

6. GIFT Nifty / Pre-Market Cues & Overall Market Open Outlook

- LiveMint: Nifty 50, Sensex today: What to expect from Indian stock market in trade on February 23

- Financial Express: How will markets open today? GIFT Nifty up, 15% Trump Tariff; silver surges 4%, gold steady and other cues