Indian markets are poised for a weak opening on February 17, 2026, as Gift Nifty signals a negative start amid mixed Asian cues and continued foreign outflows. Despite strong domestic buying and resilience in banking and infrastructure themes, global caution ahead of Lunar New Year holidays may cap early gains. Fresh analyst calls highlight selective opportunities in pharma, shipping, and rail stocks.

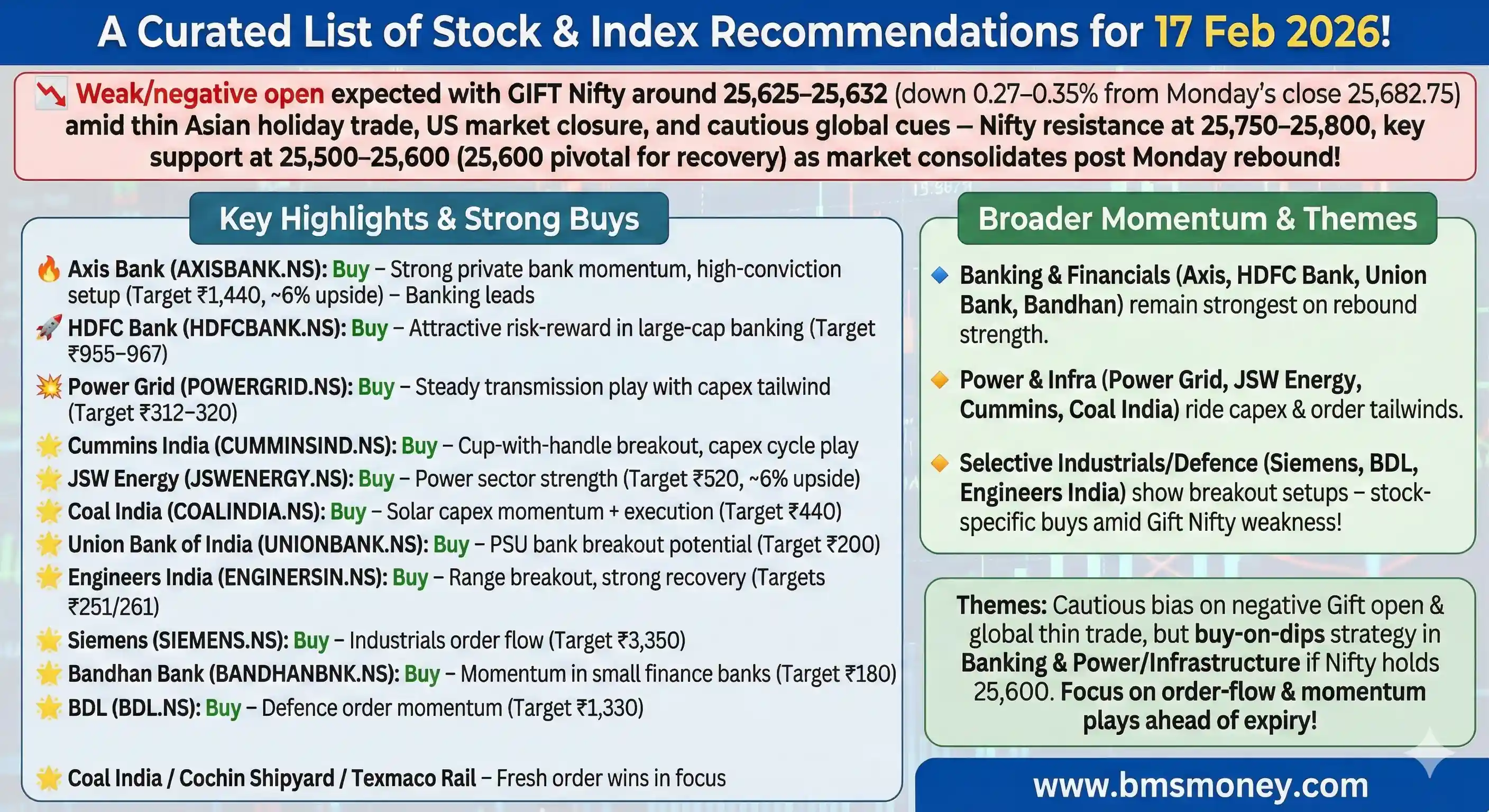

Introduction As of 8:30 AM IST on Tuesday, February 17, 2026 (a regular trading day), Gift Nifty futures are trading lower by 69–90 points (0.27–0.34%) around 25,625–25,632, pointing to a weak/negative opening for the Nifty 50 below the 25,600–25,650 zone (Monday’s close: 25,682.75, +0.83%). The Sensex closed Monday at 83,277.15 (+0.79%).

Asian markets are mixed in holiday-thinned trade ahead of Lunar New Year (Japan’s Nikkei flat-to-down ~0.2%, Hang Seng +0.5% in half-session). U.S. markets were closed yesterday. Domestic flows on Monday: FIIs sold ₹972 crore, DIIs bought ₹1,667 crore. India VIX eased slightly to 13.33.

Key themes remain banking strength, power/infra/capex orders, and selective AI/IT updates. New analyst calls have emerged since 7:30 AM, including fresh intraday buys from Chandan Taparia, Sumeet Bagadia, Ganesh Dongre, and Shiju Koothupalakkal. Stocks in focus include Lupin, Cochin Shipyard, Texmaco Rail, JSW Infra, Fortis, Fractal Analytics, and Reliance.

This pre-open update (market opens 9:15 AM IST) incorporates the latest Gift Nifty moves and fresh recommendations published by 8:30 AM.

Section 1: Index Outlook (as of 8:30 AM IST)

| Index | Outlook/Bias | Key Levels | Expected Open / Range | Key Drivers |

|---|---|---|---|---|

| Nifty 50 | Weak open, cautious bias | Support: 25,500–25,600 Resistance: 25,750–25,800 | Below 25,650 (GIFT discount ~50–80 pts) | Gift Nifty weakness, global holiday thinness, banking/infra flows |

| Sensex | Aligned with Nifty | ~82,900 / ~83,600 | Negative bias | Same as Nifty |

| Bank Nifty | Mildly positive (sector focus) | Watch 60,500–61,000 | Follow banking picks | Private & PSU bank momentum |

Nifty needs to defend 25,600 for any recovery toward 25,800; a break below 25,500 could accelerate selling.

Section 2: Sector-Wise Stock Picks (Fresh + Updated Calls)

Banking & Financials

- Axis Bank [Buy] @ ~₹1,358, Target ₹1,440, SL ₹1,320 (Ajit Mishra, Religare Broking)

- HDFC Bank [Buy], Target ₹955–967, SL ₹897 (Akshay P. Bhagwat, JM Financial)

- AU Small Finance Bank [Buy], Targets ₹1,027/1,054, SL ₹972 (Akshay P. Bhagwat, JM Financial)

- Bank of India [Buy] @ ~₹165, Target ₹173, SL ₹162 (Rajesh Palviya, Axis Securities)

- Union Bank of India [Buy] (Chandan Taparia), Target ₹200, SL ₹175 – Bullish pennant + 20-DEMA support

- HDFC AMC [Buy] (Chandan Taparia), Target ₹3,000, SL ₹2,750 – Trendline breakout

- Bandhan Bank [Buy] @ ₹167.93, Target ₹180, SL ₹162 (Sumeet Bagadia, Choice Broking)

- Canara Bank [Buy] @ ₹146, Target ₹154, SL ₹142 (Ganesh Dongre, Anand Rathi)

Power, Energy & Infrastructure

- Power Grid Corporation [Buy] @ ~₹300.5, Target ₹312 (Religare) / ₹320 (Chandan Taparia), SL ₹290–294

- Cummins India [Buy] ₹4,500–4,580, Target ₹5,250 (2–3 months), SL ₹4,280 (MarketSmith India)

- Godawari Power & Ispat [Buy] ₹266–268, Target ₹308, SL ₹254 (MarketSmith India)

- JSW Energy [Buy] @ ₹489, Target ₹520, SL ₹478 (Shiju Koothupalakkal, Prabhudas Lilladher)

- Coal India [Buy] @ ₹422, Target ₹440, SL ₹410 (Ganesh Dongre, Anand Rathi) – Also solar capex momentum

- Cochin Shipyard / Texmaco Rail – In focus on fresh orders (L1 ₹5,000 Cr & ₹219 Cr respectively)

Industrials / Capital Goods

- Siemens [Buy] @ ₹3,215, Target ₹3,350, SL ₹3,150 (Shiju Koothupalakkal)

- BDL [Buy] @ ₹1,250, Target ₹1,330, SL ₹1,230 (Ganesh Dongre)

- Engineers India [Buy] >₹227, Targets ₹251/261, SL ₹215 (Raja Venkatraman)

- Tata Steel [Buy] @ ₹205.81, Target ₹220, SL ₹198 (Sumeet Bagadia)

IT / Others

- TCS – In focus on AMD AI infrastructure tie-up

- Fractal Analytics – Prabhudas Lilladher initiates coverage with ~50% upside (despite weak listing)

- KFin Tech – Citi maintains Buy, raises TP to ₹1,385

- IRB Infra – CLSA maintains Outperform, cuts TP to ₹69

Section 3: Global & Thematic Insights Gift Nifty weakness dominates pre-open sentiment. Watch AI-related news (Infosys meet, TCS-AMD) and order-flow stocks (defence/rail/shipyard). Longer-term constructive views remain (Motilal Oswal on 12% Nifty earnings CAGR for FY25-27).

Conclusion & Disclaimer Cautious-to-negative bias at open due to Gift Nifty. Focus on banking, power, and order-driven infra names for intraday swings. Defend key supports (Nifty 25,500–25,600) before adding fresh longs.

Actionable takeaway: Prioritise high-conviction banking/power picks and use strict stops in a volatile pre-budget environment.

Disclaimer: Aggregated public analyst/media views for information only. Not investment advice. Consult a SEBI-registered advisor. Markets can change rapidly.

Sources (with direct hyperlinks)

- Gift Nifty / Opening Outlook: Economic Times Live Blog | Moneycontrol Live | Business Today

- Chandan Taparia Picks: Livemint

- 8 Intraday Stocks (Bagadia/Dongre/Koothupalakkal): Livemint Trade Setup

- Raja Venkatraman & MarketSmith: Livemint

- Religare/JM/Axis Picks: NDTV Profit

- Stocks to Watch (orders): Financial Express | Moneycontrol